As a UK mortgage borrower, you may have heard about the recent introduction of the Mortgage Charter 2023.

This significant development in the housing sector is designed to provide a framework for mortgage lending, with a particular focus on supporting homeowners who may be feeling the pinch due to rising inflation and interest rates.

But what does it mean for you?

In this article, we look at the details of the Mortgage Charter, its potential benefits, and what it could mean for your mortgage journey.

Understanding the Mortgage Charter

The Mortgage Charter is a new initiative introduced by the UK government in collaboration with the UK’s largest mortgage lenders, UK Finance, the Financial Conduct Authority (FCA), and other entities such as the Building Societies Association.

The Charter outlines a set of principles and guidelines that lenders are expected to follow when assisting their regulated residential mortgage borrowers.

The Charter was introduced in response to the pressures on households with mortgages, due to rising inflation.

It represents a significant shift in the approach to mortgage lending, setting new expectations for lenders and promising to alter the landscape of mortgage lending.

David Postings, Chief Executive of UK Finance, said

“Lenders recognise and understand this is an anxious time for mortgage customers and there is a lot of support available. Lenders have been contacting and supporting millions of customers and are working with the government and regulators to continue to deliver a range of support options for customers.”

“Anyone who is worried about their finances should contact their lender to find out what options are available to help. Contacting your lender to talk about the options available will not impact your credit score.”

Key Elements of the Mortgage Charter

The Mortgage Charter contains several key elements aimed at providing support to residential mortgage customers.

Support for Concerned Customers

If you’re worried about your mortgage repayments, you can call your lender for information and support, without any impact on your credit score. This encourages open communication between you and your lender.

Repossession rules relaxed

Under the new guidelines set by the Charter, homeowners are granted a more lenient stance on repossessions. Specifically, for those who find themselves in arrears, their homes will not be subject to repossession without their agreement, unless in exceptional circumstances, for a minimum period of 12 months.

Traditionally, lenders have been known to initiate the repossession process after a three-month period of arrears. However, those lenders who have pledged their commitment to the Charter have agreed to extend this period to a full year.

This extended grace period is intended to provide homeowners with a much-needed breathing space, offering them the opportunity to regain their financial footing.

Flexibility at the End of a Fixed Rate Deal

If you’re nearing the end of your fixed rate deal, you’ll be offered the chance to lock in a deal up to six months ahead (with the same lender). Once booked, you will be able to swap to a better deal up to two weeks before the new rate starts.

Can you move home with a fixed rate mortgage?

Options to Reduce Monthly Payments

You can switch to an interest-only mortgage for six months, or extend your mortgage term to reduce your monthly payments.

You can switch back to your original term within the first six months if you choose to. Both options can be taken without a new affordability check or affecting your credit score.

How do you repay an interest only mortgage?

Support for Switching Deals

If you’re up-to-date with payments, you can switch to a new mortgage deal at the end of your existing fixed-rate contract without another affordability check.

What is a product transfer mortgage?

Mortgage product transfer vs remortgaging

Timely Information

Lenders are committed to providing well-timed information to help you plan ahead should your current rate be about to end.

Tailored Support

Lenders will offer tailored support if you’re struggling and deploy highly trained staff to help you. This could mean extending your term to reduce your payments, switching to interest-only payments, or other options like a temporary payment deferral or part interest-part repayment.

The right option will depend on your circumstances.

Lender Support

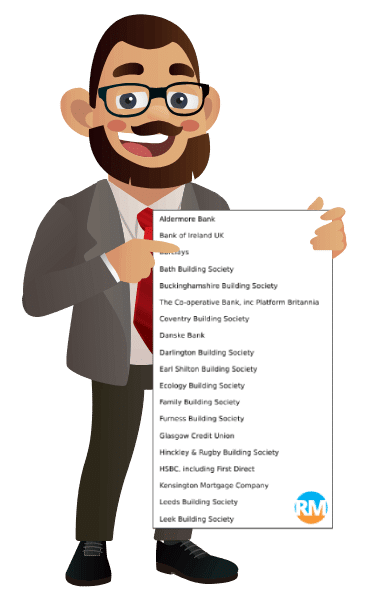

Since the introduction of the Mortgage Charter in June 2023, a number of lenders have signed up, indicating their willingness to adhere to the new guidelines.

Lenders representing 90% of the mortgage market have now agreed to the Charter, including the UK’s biggest lenders, such as Barclays, NatWest, Lloyds, including Halifax and Scottish Widows, HSBC including First Direct, Santander, TSB and Virgin Money.

Many building societies have also signed up to the Charter, including Nationwide, Yorkshire, Nottingham, Skipton, Leeds and West Bromwich.

The charter will only apply to customers of lenders who have signed up.

However, if your bank or building society is not on the list, they will offer alternative support.

Benefits for Borrowers

The Mortgage Charter aims to make the residential mortgage process more transparent, with clearer terms and conditions, and a commitment to fair treatment.

This could potentially make it easier for you to understand your mortgage agreements and navigate the home-buying process. For example, if you’re approaching the end of your fixed-rate deal, you’ll have the chance to lock in your next mortgage deal up to six months ahead.

This can provide peace of mind and help you plan your finances more effectively.

Implications for Landlords

It’s important to note that the Mortgage Charter does not extend its provisions to investment properties.

So buy to let and holiday let landlords are not included.

According to updated guidance from HM Treasury, the commitments from lenders to support mortgage holders under the Charter do not apply to buy-to-let mortgages.

This has raised concerns among landlords and investors in the buy-to-let market, who are also grappling with the challenges of rising interest rates and inflation.

Considerations When Opting for Support

While the Financial Conduct Authority (FCA) has expressed its support for the commitments outlined in the Charter, it also advises borrowers to be mindful that even temporary modifications could potentially lead to increased monthly payments in the future or a higher overall repayment amount.

For instance, if you choose to switch to an interest-only mortgage for a six-month period, it’s important to understand that this will likely extend the duration of your mortgage repayment.

During this period, you’ll only be covering the interest on your loan, without making any progress towards increasing your equity or reducing the principal amount you owe.

Sheldon Mills from the FCA, emphasised this point

“If you can keep up with your mortgage payments, you should, as changing your contract could lead to higher payments down the line.”

“But if you are worried about making your payments, contact your lender as soon as possible as they have a range of options to help.”

IF YOU NEED HELP

Please see your lender’s website in the first instance, you will find details about whether they are signed up to the Charter and the support available. If you need help with your mortgage payments, please then contact your lender in the usual ways: online, over the phone, via the app or in branch.

Final thoughts

Mortgage borrowers are under increasing financial pressure due to interest rate rises and the cost of living.

These measures will undoubtably provide some short term relief and peace of mind.

Some of the available options will have consequences down the line. Particularly where the mortgage is extended or temporarily switched to interest only payments. Both will mean that you pay slightly more interest over the remaining years of the mortgage term. And when the interest-only reverts back to repayment, the monthly cost will be higher than before.

The ability to lock in a fixed rate six months in advance is very handy, and only applies to mortgage product transfers. You can achieve the same result by remortgaging to a new lender, although this won’t have the added option of switching again, up to two weeks before the deal starts.

Product transfers (remortgage with the same lender) won’t have affordability or credit checks. Well this is how most lenders work now anyway. One of the big advantages of a transfer is that you can switch rate, regardless of your financial situation (unless you are in arrears), and there’s often less mortgage fees to pay.

Mortgage Types Guide

Not sure which mortgage is right for you? Our guide to the different mortgage types will help you to decide.

Remortgage Guide

Our Guide covers the remortgage process, including how long it takes, and the different options you have when switching your mortgage.

Mortgage Broker Guide

In this guide we’ll take a look at what mortgage brokers do, how they can help you, how they get paid plus tips on how to find a good one.