How Does Equity Release Work?

Wondering how to access the cash tied up in your home without having to sell? Equity release might be the answer you’re looking for.

Are you approaching retirement or already enjoying it, and wondering how you could boost your income or finances?

If you own your home outright or have significant equity, equity release could be the key to unlocking the value that’s been building up within your property.

Simply put, equity release lets homeowners aged 55 and over access a portion of their property’s value as a cash lump sum or regular payments.

This can provide a much-needed financial boost for various purposes – supplementing your retirement income, tackling unexpected expenses, or simply enhancing your quality of life.

Please Note: The content on this page is designed to be a helpful starting point for understanding equity release. It explores the concept, different plan types, and the general process involved. However, equity release is a complex financial decision with significant implications for your long-term financial security. To determine if equity release is the right option for you, it’s essential to consult with a qualified financial adviser who specialises in equity release products.

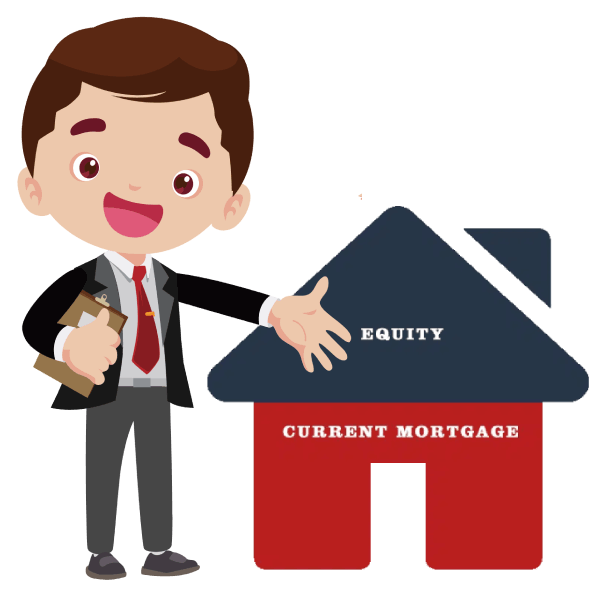

Unlocking Your Home’s Value

As a homeowner, you’ve likely built up substantial equity in your property over time.

This equity represents the portion of your home’s value that you own outright. To determine your equity, you would simply subtract any outstanding mortgage balance from your property’s current market value.

For example, if your home has a market value of £300,000, and you have a remaining mortgage balance of £50,000, your equity would be £250,000.

This valuable equity is what equity release allows you to access for your various financial needs and goals.

Accessing Cash Through Equity Release

Equity release opens up the possibility of converting a portion of your home’s value into cash in hand.

Essentially, you’re borrowing a percentage of your equity, known as the loan-to-value ratio (LTV).

Several factors influence the maximum LTV percentage you can access:

- Age: Generally, the older you are, the higher the LTV you may be eligible for. You need to be at least 55.

- Property Value: The overall value of your property plays a significant role in determining the potential release amount.

- Lender’s Criteria: Individual lenders have their own specific guidelines and LTV percentages that they offer.

One of the appealing aspects of equity release is the flexibility in how you use the extra money. Whether you dream of travelling in retirement, desire home improvements, or need help with unexpected expenses, the choice is entirely yours.

Equity Release Advice

Award winning service

Equity release experts

FCA Regulated

Let us match you with a fully qualified equity release expert.

Call us on 0330 030 5050

Repayment Options and Considerations

The most popular form of equity release is the lifetime mortgage.

With this option, you won’t face the typical monthly repayments associated with a traditional mortgage. Instead, the interest on your loan accumulates over time, a concept known as “rolled-up” interest.

This interest gets added to the total amount owed, steadily increasing the loan balance as the years pass.

While this “no-monthly-payment” structure offers flexibility, it’s crucial to understand its long-term implications.

As the interest compounds, the total debt grows significantly. This means the amount ultimately repaid from the sale of your home will be considerably higher than the original sum borrowed.

Therefore, it’s essential to carefully consider the potential impact on any inheritance you may wish to leave for beneficiaries.

Impact on Inheritance

It’s important to be aware that equity release directly impacts the equity remaining in your home and any potential inheritance you may wish to leave.

Since the interest on your equity release loan compounds over time, it gradually erodes the value of your remaining equity. The longer the equity release plan is in place, the more significant this impact becomes.

This aspect of equity release requires careful consideration. If leaving an inheritance for loved ones is a priority, it’s vital to weigh the potential benefits of equity release against the reduced amount you would ultimately leave behind.

Long-Term Impact

Equity release can be a valuable financial tool, but it carries significant long-term consequences for you and your beneficiaries.

The key factor to remember is that since you’re not making monthly payments, the interest on your loan accumulates and gets added to the total amount owed.

Over a prolonged period, this means the outstanding debt can grow considerably.

Seeking Professional Advice

Equity release is a complex financial decision with long-lasting implications.

Consulting a qualified financial adviser specialising in equity release products is absolutely essential. Their expertise allows them to comprehensively understand your situation and guide you through the available options.

A knowledgeable adviser provides invaluable support throughout the process.

They’ll meticulously analyse your personal circumstances, including your current financial situation, aspirations for the future, and your perspective on inheritance.

They’ll then simplify the complexities of different equity release plans, explaining interest rates, fees, and potential risks involved in clear terms. Ultimately, based on your unique needs and goals, they’ll help you determine if equity release is the most suitable solution or explore alternative financial strategies that might be a better fit.

We can help you find a whole-of-market equity release specialist.

FREE matching service

Call us on

0330 030 5050