credit

Your Credit Report Explained

Your credit history is a continually updated summary of your credit based activities. It will include how much you have borrowed from each provider, along with any late payments or credit defaults.

This information is combined into a Credit Report. Here we will run through what the report contains and how you can view the data to check that everything is accurate.

Understanding your credit report is an important step in maintaining your financial health. Your credit report is a record of your credit history, including information about your credit accounts (loans, credit cards, overdrafts) and payments.

This information is used by lenders to determine your creditworthiness, and it can also be used to help you track your spending and identify potential fraud. UK credit reports are maintained by the three major credit reference agencies: Experian, Equifax, and TransUnion.

By law the Credit Reference Agencies (CRA) have to provide you with a free copy of your report. If you find any errors, you can dispute them with the credit reporting agency. They then must investigate any disputes that you raise and correct any inaccuracies in your credit report.

What is a Credit Report?

Credit Reports are available from commercial organisations called Credit Reference Agencies (CRA).

In the UK the three main CRAs are:

- Experian

- Equifax

- TransUnion

Each will hold a slightly different version of your credit history as lenders don’t always provide the same information to all three at the same time.

Credit reference agencies hold information about your credit agreements (including any arrears), rent agreements, county court judgments and electoral roll information. They will also show what hard searches have been made on your account, soft credit searches are not recorded. A lender or landlord can only pass on information about your agreements to a CRA with your consent.

Your Credit Report will contain all of this information to help a prospective lender make a decision to lend, or not.

What does a Credit Report show?

A lot of the data relates to credit facilities like; loans, car finance agreement, credit cards, mortgages. This will be supplied by the banks, building societies and finance companies that you have applied to.

There’s also mobile phone companies, utility companies, payday loan providers, catalogues etc.

Plus publicly available sources such as the electoral register.

What’s included?

Credit history

A summary of your credit related accounts and how you have managed them.

Connections

This is a list of people that are financially connected to you via a joint mortgage or credit facility.

Payment profile

Repayments made on time, missed, or late are all recorded and remain for six years.

Addresses

Past and present addresses taken from the electoral roll and credit application forms.

INCLUDED

- Name and addresses

- Date of birth

- Electoral roll

- Late payments

- Missed payments

- Amounts owed

- County Court Judgements (CCJ)

- Repossessions

- Bankruptcy

- Individual Voluntary Arrangement (IVA)

- Instances of identity theft

NOT INCLUDED

- Savings account balances

- Student loans

- Employment details

- Earnings

- Property ownership

- Medical details

- Driving offences

- Religion

- Criminal record

RECORDED FOR SIX YEARS

Missed or late payments and defaults. CCJs, repossessions, bankruptcies, debt relief orders, IVAs

An IVA will show on your credit report and thus affects your ability to apply for credit during the IVA period. This article looks at what an IVA is, how it works and how long it stays on your credit report.

How long does an IVA stay on your credit report?

How Does a Debt Management Plan Affect Your Credit Rating?

Who can see this information?

When you apply to borrow money or take out a credit arrangement you will need to give permission for your credit report to be accessed.

For information to be reported to the Credit Reference Agencies (CRAs), a reciprocal data sharing agreement must be in place between the organisation reporting the data and the CRA. This means that a company reporting account information will also be eligible to see payment history reported by other lenders.

These types of companies will be quite obvious to you; mortgage lender, bank overdraft, credit card company, payday loan lender.

The less obvious ones are where you are not overtly borrowing any money; mobile phone provider, mail order company, utility companies, Sky, car PCP contracts.

The credit report information can be accessed by lenders, landlords, employers, and utility companies.

As well as basic data such as who a loan is with and how much is outstanding, your credit report will show the pattern of your payments for each provider. This can be a good indication (or bad) for a potential lender about how you look after your finances. If there are lots of late or missed payments, over multiple accounts, you reduce your chances of getting the best terms available.

In certain cases it may be necessary to approach a lender who specialises in bad credit mortgages. These will be dearer than a standard mortgage but the lenders are more understanding where credit issues exist.

How to check your Credit Report (and why)

Most people over 18 will have information held on their credit file, some more than others. It’s a good idea to check this on a regular basis to make sure the entries are accurate.

Because each of the three main credit agencies hold slightly different data it is prudent to check all three. You’ll be able to look for any mistakes or spot entries that may be fraudulent and related to identity theft.

You have a legal right to access your credit report for free from any credit reference agency. These reports will provide a snapshot of your credit history but won’t include a credit score. For a monthly fee they will provide alerts and enhanced data.

Experian

Use MSE Credit Club, which offers full access to your Experian credit report for free anytime.

Equifax

Use Clearscore, which provides free access to your Equifax report.

TransUnion

Use Credit Karma, which gives you free access to your TransUnion report.

It’s recommended that you check all three every year. It is particularly important to do this a few months before you apply for a mortgage. This will give you the opportunity to spot and put right any inaccuracies before making your mortgage application.

If you are short on time then go for Experian as they are the biggest or use CheckMyFile who can access all three on your behalf.

Checking your file and correcting errors is part of the process of getting mortgage ready. This means getting yourself, and your credit file, into the best possible shape for mortgage success.

Correcting errors

If you notice any errors it is important to get them amended asap, so that all the information is accurate and true.

Any inaccuracies will harm your credit profile and possibly affect your ability to obtain a mortgage or other credit facility. Errors can be as simple as incorrect address information. Missed payments, which stay on your account for six years, are the entry most people dispute.

To do this you can either contact the CRA that supplied the credit report, or approach the credit provider directly. This process can take some time so perseverance is key.

30 day FREE credit report trial

Get The UK’S Most Detailed Online Credit Report

See your data from 4 Credit Reference Agencies, not just 1

Get an independent view with your checkmyfile Credit Score

View up to 6 years’ credit history

Easy to cancel – by Freephone or even online

A guarantee never to sell your personal data

Consistently rated ‘Excellent’ on Trustpilot

This is a 30-day free trial, and a recurring £14.99 thereafter unless the subscription is cancelled, which can be cancelled at any-time.

Credit & debt in joint names

Where you have taken out a credit agreement with someone else, your credit file will show a link to them.

So how you conduct your financial affairs may affect them and vice versa. Typically this association would come from a joint mortgage, joint loan agreement or possibly where someone has agreed to be a guarantor.

Trying to get a joint mortgage when one person has some bad credit will affect the overall application, and may cause it to be rejected.

Once you no longer have any connection with the other person you can ask the Credit Reference Agencies to disassociate you from them, effectively removing the link.

This can only be done once the credit agreement has been settled and you no longer live together.

You will find more useful information in our Guide to Divorce and Mortgages.

How to improve your credit profile

If you’re looking to improve your credit profile, there are a few things you can do to make it happen.

Here are some tips to get you started:

DO

- Make all of your credit card and loan payments on time. This will show lenders that you’re a responsible borrower.

- Keep your credit balances low. High balances can indicate to lenders that you’re overextended and may have trouble making payments.

- Limit your applications for new credit. Each time you apply for credit, it shows up on your credit report as a hard inquiry. Too many hard inquiries can hurt your credit score.

- Check your credit report regularly for errors and dispute any that you find. inaccuracies on your report could lower your credit score needlessly.

DON’T

- Apply for payday loans. They are an obvious sign that your finances are struggling.

- Take all of your credit cards up to their limits. Again, this shows that money is tight.

- Only pay the minimum amount requested by your credit company each month.

- Miss any payments. This will damage your credit score and make it harder to get approved for new financing.

- Keep applying for different styles of credit.

- Neglect your credit report. Checking it regularly for errors is an important part of maintaining a good credit score.

DEBT ADVICE

You will find that your mortgage broker can provide a level of advice concerning managing debt and not overextending yourself.

If you are still struggling then it’s probably a good idea to touch base with a debt management specialist:

Citizens Advice – Dealing with money issues can sometimes be off-putting, but if you don’t understand how things like credit or mortgages work, you could end up losing out financially or getting yourself deep in debt. Citizens Advice will give you the information you need to make the right choices, including help to deal with your debt problems, how to avoid losing your home and how to get your finances back into shape.

https://www.citizensadvice.org.uk/debt-and-money/

StepChange – is the UK’s leading debt advice charity. They help hundreds of thousands of people each year deal with their money worries with free, impartial and non-judgmental advice.

Do you have a thin credit file?

A thin credit file is a term used to describe a person who does not have a lot of credit information stored about them.

This can be problematic because it can be more difficult for thin credit files to get approved for loans and other lines of credit.

This is an issue for lenders because they have no way to assess the risk of lending to someone with little to no credit history. There is no pattern of applying for credit or making the required repayments.

By looking at your own credit file, and perhaps seeking advice, you can see if your profile is a bit ‘thin’ and work towards changing this.

Read more – What is a thin credit file?

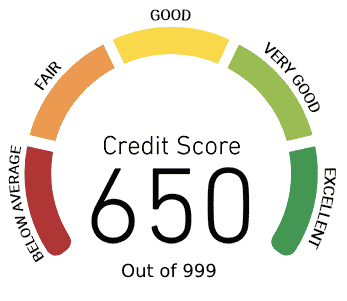

What is a Credit Score?

A credit score is a calculated number that reflects your credit history, behaviour and creditworthiness and is separate to your credit report.

Think of it as a combination of everything noted on your credit file, represented as a number.

It’s used by lenders to decide whether to approve you for a loan or credit card, and at what interest rate. Your credit score is based on factors like how often you make payments on time, how much debt you have, and how long you’ve had credit accounts.

A high credit score means you’re a low-risk borrower, which could lead to lenders approving you for a loan or credit card and possibly with a lower interest rate. A low credit score could lead to higher interest rates and could mean you’ll be refused some types of credit.

Your score can range from 0 up to 999. (0 is bad)

Credit scores are provided by each credit reference agency and so they will all be slightly different. Your checkmyfile credit score is based on all of the Credit Report information they gather from Equifax, Experian, TransUnion and Crediva.

What credit score is needed for a mortgage? Lenders will use different systems for working out your score. They won’t tell you what score they hold for you but they do have to disclose which credit agency they use if you ask.

You are able to influence your credit score, afterall it is based on the credit you have applied for and how you pay it back.

Try to :

- Pay all of your bills on time

- Pay your rent or mortgage on time

- Don’t spend up to your credit limit/s

- Reduce the number of credit agreements you apply for

- Don’t take out cash on credit cards

- Fix any errors on your credit report

- Ensure that the overall amount of unsecured debt is decreasing each month

FAQ

Frequently Asked Questions

Are credit reports confidential?

Yes. You need to give your permission before anyone can access your credit file.

How long is a credit report valid for?

It will change frequently, recording new payment information, balances and new enquiries.

How far back does a credit report go?

Your credit file is a record of how you have managed your finances over the previous six years.

Why is my credit score low when I have no debts?

You may have a thin credit file because you have not applied for much or any credit facilities. This makes it hard for lenders to assess you.

What is a default?

A default occurs if a lender decides to close your account because you’ve missed the contractual payments.