Self-cert (self-certification) mortgages were once popular in the UK, but they are no longer available. This type of mortgage was particularly attractive to self-employed borrowers because it allowed them to certify their own income without having to provide any documentation.

However, since the financial crisis of 2008, lenders have been much more cautious about who they lend money to and have tightened up their lending criteria. Additionally, the FSA/FCA introduced rules which ultimately led to the demise of self certification mortgages.

What is a self-cert mortgage?

A self-cert mortgage was available to any type of borrower who found it difficult to prove their actual income. Providing there was enough equity in a property, lenders allowed the borrower to declare their own income without having to provide any documentation.

So basically you filled in a box stating your gross annual income and signed to say that this was true!

Job done

The main advantage of a self-cert mortgage was that it was easier to qualify for than a traditional mortgage and quicker to underwrite. This is because the borrower did not have to provide any actual proof of what they earned and the lenders did not need to check them.

The slight downside of a self-cert mortgage was that it was more expensive than a traditional mortgage and the maximum loan to value tended to be restricted to around 70%-75%.

Why aren’t self-cert mortgages available anymore?

The ability to self declare your own income was frequently misused and also led to borrowers taking on levels of debt that they really could not afford. In 2010 the Financial Services Authority, who at that time regulated mortgages, put forward new rules whereby all new mortgages had to pass affordability checks with full proof of income.

The new rules made it much harder for borrowers with complex income situations to get a mortgage.

Self-cert criteria applied to both residential mortgages and buy to let mortgages. This enabled property investors to obtain an almost unlimited number of buy to let mortgages, without needing to prove their income position.

The financial crash of 2008 also uncovered problems within property investments where property prices were inflated, or overstated, just to allow for higher borrowing. A lack of basic checks and common sense gave buy to let investors the green light to borrow hard and fast.

The popularity of self-cert

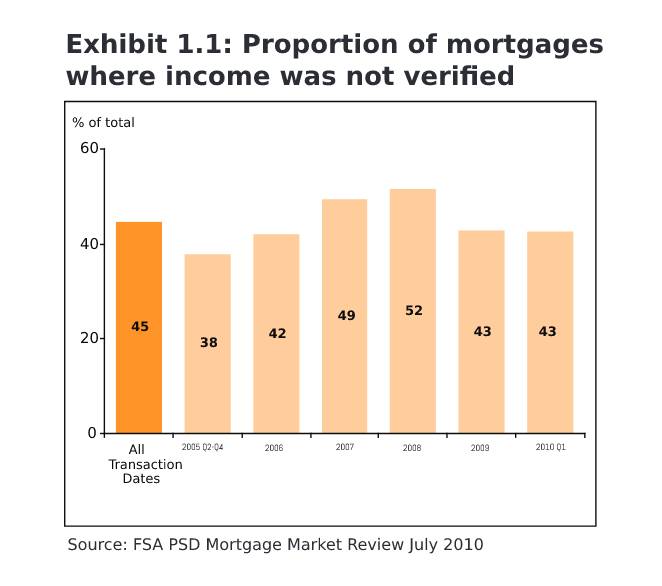

According to the FSA Mortgage Market Review, in April 2005 to March 2010, income was not verified on 45% of all new mortgages.

This includes fast-track applications, where lenders choose not to request proof of income for certain low risk loans below 75% LTV.

Even in 2010, 43% of mortgage applications were processed without any income checks.

Who would have used this type of mortgage?

Self-certification mortgages were most popular with self-employed people, particularly those who had recently started their business or were not up to date with their accounts. This is because they often found it difficult to provide proof of income.

It was also popular with people with irregular incomes, such as freelance workers or people who worked on commission or subcontractors.

Borrowers with multiple sources of income, such as those with a portfolio of properties or multiple business interests, often found it easier to self-certify their income. It was a great time saver for the right person.

But there were also some who just took advantage of the situation and made up an income figure so that it justified the loan amount. (yes, they really did).

What are the alternatives?

There’s no direct alternative for a self-cert mortgage. All mortgage lenders must now receive evidence of a borrower’s income with each application.

Fortunately, experienced mortgage brokers can provide solutions by working with flexible mortgage lenders who understand how self-employed income and complex income works. Finding one of these niche lenders can be tricky, but an experienced and knowledgeable broker will have relationships with these lenders allowing you to access the finance you need.

Lender’s have been able to improve their criteria to provide practical solutions for sole traders, company directors, self-employed, contractors and freelancers, along with complex income situations. Subcontractors working in construction will have access to specialist CIS mortgage schemes.

What counts as complex income?

From a lenders perspective ‘complex income’ is any situation that deviates from the standard or the norm. Having complex income will normally involve receiving your income from more than one source and some or all of it is variable and not guaranteed.

There are a number of types of income that can be considered complex:

Multiple sources of income – if you have multiple jobs or businesses, are self-employed and also receive dividends, pension income or have retained profits in your business.

Seasonal income – if your income fluctuates throughout the year

Overseas income – if you’re paid in a foreign currency or earn money from overseas

Retired with income – if you’re retired but still receive pension income and investment income

What proof of income is now required?

All mortgage applications now need you to include proof of your income.

The requirements for this are:

Employed

- 6 months payslips

- Most recent P60

- Bank statements

Self-employed/Complex

- Sole trader accounts

- Company accounts

- Personal SA302 calculations

- Bank statements

- CIS payslips

It’s normally OK to provide scanned/pdf copies for proof of income and bank statements. Originals are often needed for proof of ID such as your driving licence and passport.

Your mortgage broker will check that you have all the right documents before you apply to the lender. The aim is to submit your application without any errors or missing documents.

How many years of self-employed accounts do you need?

So in an ideal world you would be able to provide three full years of trading accounts, along with SA302. This gives the lender a good idea of how your income averages out over that time.

But what if you don’t have three years of trading yet?

By working with a mortgage broker you can access lenders that don’t need the full three year history. You’ll still need to demonstrate affordability, and have a decent deposit.

How can a mortgage broker help?

Specialist mortgage brokers have access to a wide range of mortgage lenders, many of whom offer solutions for clients with complex incomes. A lot of these niche lenders only work with brokers, so you are unlikely to even find them if you try to go it alone.

A good mortgage broker will also have an in-depth knowledge of the different types of evidence required by each lender and how to present it in the most effective way. This can save you a lot of time and hassle when it comes to applying for a mortgage.

If you’re self-employed or have a complex income structure, then speaking to an independent mortgage broker is a good first step in finding the right mortgage for you.

Not on the High Street!

The high street lenders can’t help every mortgage customer and they prefer the simple, low-risk ones.

If your situation is a bit different or needs a more personalised solution then our brokers can help.

Expert advice, for all situations.

Bridging Loans

The most flexible of secured loans and often misunderstood. Bridge loans can be used in so many different ways and can be arranged super fast.

Large Loans

High net worth mortgage brokers understand complex large loans and unique situations and can source bespoke deals from the right lenders.

Let to Buy

Let to buy combines a buy to let remortgage with a residential mortgage. Allowing you to move house while keeping your current home.

More articles

Mortgage Guides

Comprehensive and expertly written mortgage guides