If you are looking to buy a home but don’t have enough deposit yet, then a family offset mortgage could help you out.

These are popular with first-time buyers, but available to anyone moving house.

A family offset mortgage, or parent offset mortgage, works by linking your new mortgage with savings from family members. Our guide explains how these mortgages work, including the benefits and availability.

What is an offset mortgage?

An Offset Mortgage uses any cash savings that you have to ‘offset’ the interest charged on the mortgage balance.

This has the effect of reducing the mortgage interest payable to the lender and so makes your mortgage a little cheaper.

They work by looking at the combined balances in your mortgage account and your linked savings accounts each day. The savings amount is deducted from the mortgage amount, leaving a lower figure.

This net amount is then used to calculate the amount of interest due for that day.

While you won’t earn any interest on your savings, you won’t be charged any interest on the same amount of money in your mortgage.

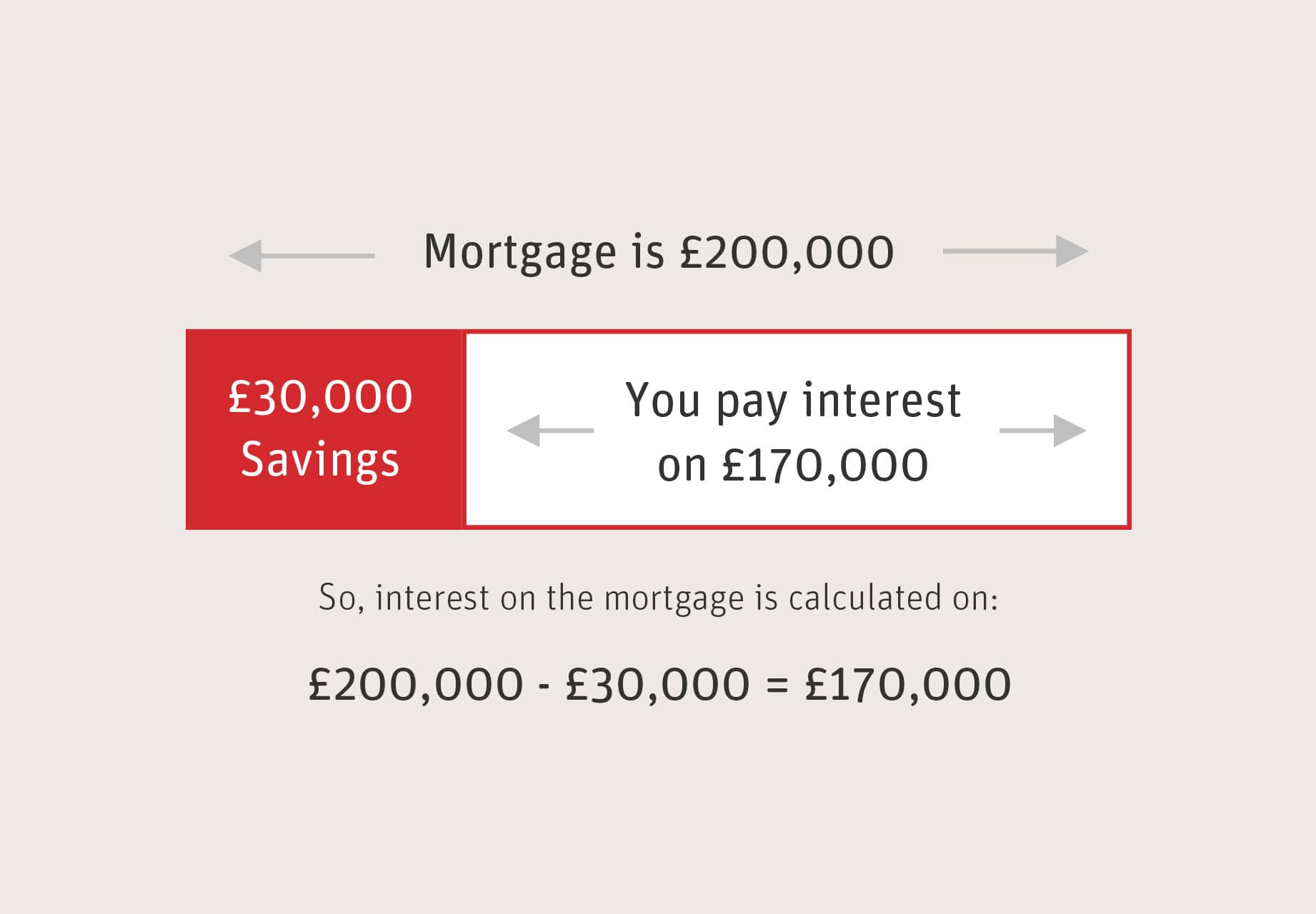

Any money you deposit remains in separate accounts, so you always have instant access to your cash. However, they are linked by the lender which means you only have to pay interest on the difference between the amount in your savings and the outstanding mortgage.

So if you have an offset mortgage for £200,000 and £30,000 as linked savings you will only pay interest on the difference, £170,000.

How does a family offset mortgage work?

A family offset mortgage works in the same way, but a family member (who is not formally part of the mortgage) uses their savings to provide the cash for offsetting.

Like a normal offset, a parent offset mortgage reduces the loan amount on which mortgage interest is calculated. Reducing the amount of interest you have to pay.

While it’s most common for a parent to provide the cash savings, they can be arranged with other family members too. And some lenders will allow multiple family member to help, pooling their cash savings to offset more interest.

With a family offset mortgage, a family member links their savings to your mortgage.

Do you still need a mortgage deposit?

Whether or not you still need to provide a cash deposit will depend on the lender.

Some family deposit mortgages will allow the family savings amount to be used as a deposit. This no deposit option does not need any cash from the borrowers.

Others require you to have at least 5% saved up, in addition to any family help.

Mortgage eligibility

Even though your family are putting up their cash savings to help you, there’s still a need for you to satisfy the lender’s eligibility requirements.

As the borrower, you are fully responsible for making the monthly repayments each month.

This means that you have to meet the lender’s criteria when applying for your mortgage.

Income

You need to have a regular, provable income. Whether you are employed, or self-employed, expect the lender to ask for payslips, P60, SA302, accounts, bank statements etc.

Affordability

Having a good income is only part of the equation. The lender also wants to find out what you spend it on! They will need to check that you can afford the new mortgage, alongside your normal living expenses and financial commitments.

Credit history

It’s important for all borrowers to have a satisfactory credit history, and hopefully no bad credit. You can check your own status by getting a copy of your credit report. If you spot any errors then get these fixed asap. If you haven’t previously applied for any credit then you may have a thin credit file, which poses it’s own problems.

Property

The property you wish to buy needs to be acceptable to the lender. Issues with short leases, non-standard construction or properties that are near to commercial businesses can be off limits for some lenders.

Deposit

Putting down your own deposit is always beneficial, as it reduces the size of your mortgage. But not all lenders require you to do this. Some will use the offset savings as a form of deposit, which will also lower your loan to value LTV.

Family members

Some lenders have strict rules concerning ‘who’ can help you, while others are more relaxed. If the money is not being provided by your parents then it’s important to confirm that this is OK.

How much savings do you need?

There’s no simple answer to this question, it just depends.

Offset mortgages don’t generally have the most competitive interest rates, so there has to be a trade off.

Equally, a family offset mortgage could allow a first time buyer to get on the property ladder, which for many FTB’s is priceless.

How much is needed will depend on the property you wish to buy and how much cash savings your family is prepared to use.

Probably 10% of the purchase price is a bare minimum to get started with.

Don’t forget about the other costs!

While the mortgage deposit is unquestionably the largest cost of buying a home. Don’t forget to budget for the other costs.

These could include:

Legal fees

Stamp duty

Survey fees

Broker fees

Main benefits

The main benefit of a family offset mortgage is that it enables homeownership to happen that much sooner.

It can fast-track the buyer onto the property market, reducing the usual delay associated with saving up the cash deposit.

For parents, it allows them to help their children buy a home, without having to gift the money to them permanently.

Mortgage deposit

The offset money can reduce the need to save for a mortgage deposit, and in some cases replace it completely.

Lower interest

As the money in the savings accounts is used to offset the borrowed money, it means the mortgage interest charged is lower than without the savings,

Smaller repayments

Offsetting can be used to reduce the monthly mortgage repayments, making the mortgage more affordable.

Cash is returnable

With an offset mortgage arrangement, any cash savings used will be returned to it’s owner. Although this may take many years to happen.

Lower LTV

The savings element effectively means that you don’t need to borrow as much from the lender. This lowers the loan to value percentage, making it less risky for the lender, and could allow you access to some better deals.

Tax efficient

Where the family member is a high rate tax payer, offsetting gives another benefit. As they will not be ‘earning’ interest on the offset money, there’s no income tax burden. So the interest saved is tax free.

Offset options

All offset mortgages use the linked savings accounts so that you are charged less mortgage interest.

This saving can be used in one of two ways:

Reduce your payments

You would use the savings in mortgage interest to automatically reduce your monthly payments. The mortgage term stays the same but you pay less each month. The benefit changes according to the amount of linked savings.

Reduce your term

You keep your monthly payments at the ‘full’ level and the interest that has been offset then goes against your mortgage balance each month. This is a form of overpayment and will reduce your mortgage term, paying the debt off quicker.

What’s the difference between a mortgage deposit and an exchange deposit?

Most people are familiar with the mortgage deposit. This is the sum of money that you have saved and intend to use to help purchase the property. But when exchange of contracts takes place your solicitors will need an exchange deposit and the amounts of money will not necessarily be the same!

Alternatives

It’s fair to say that a family offset mortgage is not right for everyone. At it’s heart is the need for a family member to have sufficient cash savings to be eligible.

If an offset mortgage isn’t a good fit for you, then there are some alternative options:

Gifted deposit

Rather than using an offset mortgage, your parents could just gift you the deposit instead. This gift is non-returnable and the lender is likely to ask for this to be confirmed in writing.

Equity release

By releasing equity from their home, your parents could provide you with a gifted deposit. The most popular equity release plan is a lifetime mortgage.

Family deposit mortgage

If your parents are unable to use cash savings, they could use the equity in their own home to help via a family deposit mortgage.

Joint mortgage with parents

It is possible to have a joint mortgage with your parents but this would mean all of the borrowers would also be owners of the property. The options below may be a better solution.

Guarantor mortgage

A guarantor mortgage allows someone else to be part of the mortgage (along with you) so that you qualify to borrow a higher amount.

Joint Borrower Sole Proprietor (JBSP)

Joint Borrower Sole Proprietor is the new improved version of a guarantor mortgage. It is designed to help borrowers improve mortgage affordability by adding one or both parents to the application as joint borrowers but without adding them to the property deeds as owners.

Concessionary purchase mortgage

A concessionary purchase is where a property is sold for less than it’s true market value. A common scenario would involve a parent selling to a child or a landlord selling to their tenant.

Disadvantages

A family offset mortgage won’t be suitable for all borrowers.

Here are some of the disadvantages:

Not always the best interest rates

The main benefit is the ability to offset savings. The interest rate choices are not always the most competitive, and you may find better ones by using a regular cash deposit.

Limited choice

There aren’t that many offset mortgages to choose from, and even less that offer family offsetting. We would hope to see this type of mortgage grow in popularity over the coming years.

No savings interest

Family members who put their money into an offset account won’t normally receive any interest back.

Access to savings

Most family mortgage lenders use the offset money as a way of reducing the loan to value. This means that access to the savings will be restricted, until the property value has increased sufficiently.

Amount of savings

You will need a certain amount of money to qualify for these mortgages, and for them to be worthwhile. Probably 10% of the property purchase price is a good place to start.

First Time Buyer Guide

We have written this guide to show you the process of buying your first home with a mortgage.

Applying For A Mortgage

We explain what happens at each step, including what documents are needed and how a broker can help.

Mortgage Broker Guide

In this guide we’ll take a look at what mortgage brokers do, how they can help you, how they get paid plus tips on how to find a good one.

How to find the best deal

There’s a good number of lenders that offer standard offset mortgages, but not so many that allow family to provide the savings.

There’s also some schemes that allow a family member to help with a house purchase but not necessarily by offsetting.

An experienced mortgage broker can walk you through the various options and then explain which one would be the best fit for you.

Let Respect Mortgages get you matched with a specialist mortgage broker today.

Call us on 0330 030 5050 or complete the form below.

Ready to explore your options?

If you’re on the cusp of starting your mortgage journey and could use the guiding hand of a professional, don’t hesitate to reach out to a reputable mortgage broker.

They will make the process smoother and more profitable than going it alone. And remember, knowledge is power.

The more you know, the better decisions you can make. Keep reading, keep asking questions, and keep moving forward on your journey.