Trying to get to grips with the different types of life insurance can be a real bind.

There’s no shortage of jargon or confusing terms: sum assured, terminal illness, term assurance.

In this guide we are going to show you how a level term life insurance policy works and why they are one of the most common types of life policy.

What is level term life insurance?

A level term life insurance, also known as level term assurance (LTA), is an insurance policy that provides a lump sum payment if death occurs during the policy term.

This money can be used to settle a mortgage, or other debts, or to provide some financial security for family members.

It’s a no-frills policy where the death benefit (sum assured) and monthly premiums remain level throughout the policy duration.

Level term assurance is one of the most popular types of life cover, due to its simplicity and affordable premiums.

Key characteristics

Level sum assured/death benefit

Fixed monthly premiums

Fixed term in years

No cash value

How does level term insurance work?

The principle of life insurance is very simple. If you die during the policy term then the insurance company will pay out the death benefit to your family.

A level term insurance has two defining features:

The death benefit

Also known as the sum assured (not sum insured).

This is a tax-free cash lump sum that the policy will pay out in the event of a death claim. The amount remains level throughout the policy term.

The term

The term is the number of years that the policy is to last for. This is set at the beginning, and so the life of the policy is pre-determined and finite.

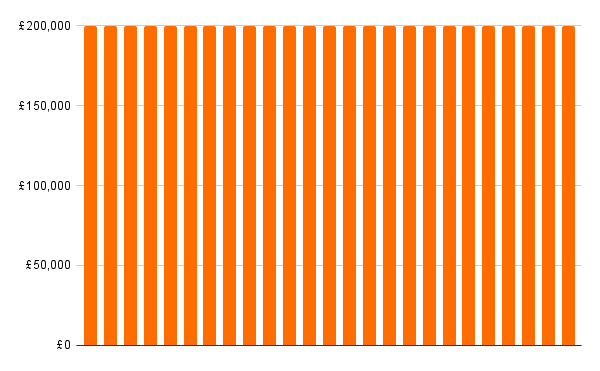

Quick example: Let’s say that you take out a policy for £200,000 death benefit, over 20 years, with a premium of £20 per month.

If you died in the first year then the insurer has to pay out £200,000. If you die in the last year they still have to payout £200,000.

Your premium won’t change and will be £20pm from the very first payment to the very last.

Let’s continue to look at how this insurance works

Sum assured

The sum assured is why you buy a life insurance policy. It is the amount of money that will be paid out if death occurs within the policy term.

There’s no set sum assured. Each person will have their own amount of money that is needed. Perhaps to repay a mortgage, for future school fees or to establish a family nest egg.

Term

You will also need to work out how long you want the cover to last for (in whole years).

The minimum is one year, and the maximum will depend on your age, but most term policies need to end by around age 90.

Premium

You will pay a monthly premium to the insurance company for the cover selected. This will be a level premium, which will not change during the policy term.

If you stop paying the premium then the policy will stop, along with the life cover.

Cash value

Term insurance policies do not accrue a cash value.

So you will not receive any money if you cancel it or try to ‘cash it in’.

Freedom to cancel

The insurer is obligated to provide the life cover for the full duration of the policy, so long as you make the payments.

However, you are able to cancel at any point and are not tied into the policy.

Just remember that the life cover ends when the policy ends.

When can you make a claim?

Death

If a life assured dies during the policy term then the insurance company will pay out the sum assured/death benefit. If there is a joint policyholder then the money will go to them, otherwise it will go into the deceased estate.

Terminal illness

A terminal illness option is standard for most term policies now. It allows you to claim on the policy ‘early’ once you have been diagnosed with a terminal illness and have been given less than 12 months to live. Once paid out, the policy will then end.

Critical illness

Critical illness is an optional extra for some term policies, and allows you to add an extra level of cover, for a higher premium. The policy will then pay out the critical illness sum assured if you are diagnosed with one of a specific list of severe illnesses or conditions. All policies will cover; cancers, heart attack and stroke as a minimum.

Can you add life insurance to your mortgage?

Taking out a mortgage involves lots of options and choices. One question that frequently arises among homeowners and potential buyers is, “Can you add life insurance to your mortgage?” In this article, we explore this topic in detail, examining whether it’s possible to add life insurance to a mortgage, the pros and cons, and alternative options you might consider.

Policy options

Most insurers will offer you different options, or riders, to enhance your cover. They won’t all offer the same, but some common policy options are:

Terminal illness cover

If it’s not already included, you may be able to add terminal illness cover to your policy.

Critical illness cover

Many insurers will allow critical illness protection to be added, sometimes this will be for the same level of cover as the life part, sometimes it can be different.

You may also be able to choose if critical illness is paid out in addition to life cover, or instead of it.

Guaranteed Insurability Option

The Guaranteed Insurability Option (GIO) will allow you to increase your life assurance when specific life events occur. These are normally; marriage, increase in mortgage, birth of a child.

Importantly, you won’t have to disclose your medical details when exercising this option.

Waiver of premium

This can be called a few different things, but it’s basically insurance for your policy premiums in the event that you are unable to work.

So if you are involved in an accident, or suffer an illness, and are now unable to work, the waiver of premium option would pay the monthly life insurance premiums for you.

For the entire policy term.

Indexation

This kind of goes against our ‘everything is level’ theme!

The problem with having level life cover is inflation. A payment of £200,000 will be worth less in 10 years time due to price rises and inflation.

So some companies allow you to opt for an annual increase in cover. This will help to fight the effects of inflation but it will also mean your premiums will rise to pay for the extra cover.

Some common uses for level term life insurance

There aren’t that many rules about what you can use life cover for. As long as a financial loss or need can be proved, then a policy can be taken out to cover it.

For the most part, these needs have a time limit. Like the term of a mortgage, or for children to attain age 21/25.

Here are a few common uses, but these are just a chosen few.

Protect a mortgage

A level term life policy is mostly used to protect an interest-only mortgage. As the mortgage balance will remain level under an interest-only loan, it makes sense to have level life insurance to match.

But in fact a level policy can be used to protect any type of mortgage; repayment, interest-only or part and part.

If used to cover a repayment mortgage then the policy still pays out the full sum assured on death. Leaving some additional funds for your loved ones.

family protection

The most popular choice for family protection.

A level term policy will pay out a tax free lump sum if you die during the policy term. Where this is on top of mortgage cover, your family will have the additional security of a lump sum to fall back on.

This could be earmarked for university fees, funeral costs, or to provide future security.

to cover debts

We’ve already explained how this policy can be used to protect a mortgage.

But in fact it can be used for any type of debt. These could include: second mortgages, credit cards, personal loans, loan guarantees, car finance, leasing etc.

The policy can be set up to match the debt. So if you have a 5 year car loan, or a 5 year lease agreement, you can have a term policy just for 5 years.

business insurance

On one level these policies can provide funds for the business if a partner or ‘key person’ passes away.

This would be Keyman Insurance or Shareholder Partnership protection insurance.

It can also cover commercial mortgages, bridging loans and any other type of business borrowing.

Alternatives

Level term assurance is very affordable and can be used in a variety of different ways.

But what if you need more, or less.

What are some alternatives to level life cover?

Decreasing life cover

If you don’t need, or want, level life cover then a decreasing life policy could be what you’re after.

It comes in two flavours:

Mortgage related: A mortgage protection life insurance automatically reduces the sum assured each year, roughly in-line with the balance on a repayment mortgage.

Non-mortgage related: These policies reduce the sum assured by a set percentage each year.

Whole of life cover

Whereas a term policy is set up for a specific number of years (the term). A whole of life policy will last, the whole of your life!

There’s no set end date, so you get long term life cover. But the premiums won’t be fixed and so you will pay more as you get older.

Increasing cover

You could have this under a term policy or whole of life. Perhaps you want a death benefit that goes up each year, to try and combat the effects of inflation.

Family Income Benefit

Not strictly a true alternative to level term cover, but a Family Income Benefit (FIB) policy is super helpful in providing extra family protection, once you’ve covered the basics.

It is designed to pay out an income, not a lump sum, upon death. So it could be used to replace an income or provide monthly payments for school or university fees.

Single or joint policy

An additional consideration when setting up a life policy is whether to go for a single policy or a joint policy.

This relates to who is covered by the life insurance under the policy.

Single life policy

Under a single policy, there is only one life assured.

The plan will only pay out the death benefit if this person dies during the policy term.

The payment will be made to their estate and then the plan ends.

Joint policy

With a joint policy, there are two lives assured. So the plan will pay out the death benefit if either person dies during the policy term. If a claim is made then the policy stops at that point, it will only pay out once.

With a joint life, first death policy, in the event of a claim the policy proceeds are simply payable to the surviving policyholder. And as that surviving policyholder is now the sole legal owner of the policy, payment can be made without the requirement of probate.

Which is better?

Where there are two people who need life insurance there’s a choice to be made:

- A joint policy, covering both lives

- Two single policies covering each person individually

A joint policy will be cheaper than two separate policies but it will only pay out once. Whereas, with two single policies there is the possibility of claiming a second time, should the surviving partner die during their policy term.

You also have more flexibility with two policies as they can have different sums assured and different terms, also different options.

Joint policies make claiming a little easier. As the surviving policyholder is now the sole legal owner of the policy, the death benefit can simply be paid to them, avoiding the need for probate.

However, we have a little trick that can improve the death payment for single life policies.

It’s called ‘life of another’.

This is a nifty option which needs two people for it to work.

With ‘life of another’ you are basically taking out a policy to cover someone else, but not yourself. So you own the policy and the other person is the life assured. (You obviously need their permission for this!)

The big advantage here is that although only one person is covered against death, the policy pays out the money to the policyholder. This makes claiming a lot quicker and does not put the sum assured value into the deceased’s estate.

How to apply

A lot of the time life cover gets sold with the monthly price being the main priority.

But unless you are able to compare this figure to the cost of other policies you won’t really know whether this is a good deal or not.

A financial adviser or broker will be able to compare the costs between many different companies, so you can be assured of getting a competitive deal.

In addition, they can help with advice concerning policy options such as:

- The amount of cover

- Critical illness

- Waiver of premium

- Indexation

- Single or joint

- Life of another

- Putting a policy in to trust

No. The payments from a level term life insurance policy are not taxable and the money can be used for any purpose.

Yes, your premiums are fixed and guaranteed to stay the same unless you alter your policy.

Level term assurance is an affordable way to protect a mortgage or your family. Premiums are affected by your age, your medical history and how much cover you need.

Yes, decreasing cover policies are available should you wish to protect a repayment mortgage.

Term life insurance plans have a fixed term. When this ends, the policy and all associated cover, will stop. It will not have a cash value.

Most insurers do now include terminal illness insurance as a standard feature of policies. However, if this is important to you, you should check the policy cover before making an application.

Once a death claim has been validated, and the sum assured has been paid out, your family is free to spend the money however they wish. Although many policies are to protect a mortgage, there is no compulsion to use the money for this purpose.

Yes, and no.

You can only take out life insurance if you have a proven insurable interest. This means that you, or someone else, will stand to lose out financially if the people covered died.

You can take out a policy on your own life without proving insurable interest. However, insurers may ask further questions if the level of cover is very high.

If you are married or in a civil partnership then you can insure each other and there’s no need to prove insurable interest.

Where you want to insure someone on a life of another basis, insurable interest will need to be established for the amount of cover you want.

Yes.

Most level term assurance, or mortgage protection, policies will need to be set up for 5-40 years.

Occasionally, there may be a need to arrange some short term life cover, for just a few weeks or a few months.

This could be because you have taken out a large short term bridging loan, or perhaps you are in-between jobs and temporarily without the employers death in service life cover.

A financial adviser will be able to arrange short term life cover, which are normally only provided by specialist insurance companies.

Yes. There is no requirement for you to be employed or working to apply for life insurance.

You may find this interesting: Can you get life insurance if you don’t work?