insurance

Mortgage Life Insurance

Mortgage Life Insurance is a specialised form of insurance designed to pay off your mortgage should the worst happen, offering peace of mind to you and your loved ones.

In this section we cover the different policies and options that can protect your mortgage in the event of your death.

Homeownership is a significant achievement, but it also represents a substantial financial obligation—your mortgage.

While it’s not something we like to think about, the question of what happens to that debt in the event of your death is an important one. This is where Mortgage Life Insurance comes into the picture.

Mortgage Life Insurance is a specific type of life insurance policy designed to settle your mortgage debt should you pass away. The money can be used to pay off your mortgage balance, relieving your family from the financial responsibility and allowing them to retain ownership of the home.

Why This Matters

For many UK homeowners, a mortgage is the largest debt they’ll ever incur. The idea of leaving this financial obligation to your family can be distressing. Mortgage Life Insurance serves as a financial safety net, designed to cover your mortgage debt.

What You’ll Learn

In this section, we’ll focus exclusively on how Mortgage Life Insurance works to cover your mortgage debt in the event of your death.

What is mortgage life insurance?

Mortgage life insurance is a type of policy that pays out a lump sum of money when one of the policyholders dies.

Normally set up as a term insurance policy, you pay a fixed amount each month and the cover lasts for a set number of years.

This would normally be the same as your mortgage term.

The purpose is for the policy to payout enough money so that the mortgage can be completely repaid.

You will find more useful information in our article: “Does life insurance have to pay off debt?“

Do you need life insurance for a mortgage?

You may be surprised to learn that having life insurance for a mortgage is not compulsory.

The choice will be up to you.

Mortgages aren’t automatically covered by life insurance, so you will need to decide what to do.

In the event of your death the full mortgage debt will need dealing with by your family. Without any cover, they will need to keep making the monthly repayments.

Likewise, if you have a joint mortgage and one person died, the surviving partner would be solely responsible for the mortgage.

Can you get a mortgage without life insurance?

Yes, you can certainly get a mortgage without taking out any life cover. The lender’s can’t make you take insurance out, nor can they make it a condition of approving a mortgage. Many people think it’s mandatory to have life insurance with a mortgage, but the only type of insurance you are obligated to take out is buildings insurance.

Can you get life insurance if you don’t work?

Yes, it is possible to get life insurance even though you are not working. You can read more about this.

Types of mortgage life insurance policy

There are two main choices when it comes to protecting your mortgage, and both are a type of term assurance.

Decreasing mortgage life insurance

The death cover reduces each year, so it is most suitable for protecting a repayment mortgage.

Fixed monthly premiums

Fixed term

No cash value

Repayment mortgage

Interest-only mortgage

Level mortgage life insurance

The death cover stays the same (level) each year, this policy can protect any type of mortgage.

Fixed monthly premiums

Fixed term

No cash value

Repayment mortgage

Interest-only mortgage

What’s the difference between life insurance and mortgage life insurance?

There’s not really much difference.

The basic underlying policy is the same. The difference is generally how they are labelled or marketed and some insurers apply slightly different underwriting rules for non-mortgage related cover.

If you bought a 25 year level mortgage term insurance, the amount of cover (sum assured) would be the same as for a level term insurance policy.

Guaranteed Insurability Option (GIO)

Some policies include a Guaranteed Insurability Option as standard. For a mortgage related policy, this would allow you to apply for extra cover should you increase the size of your mortgage.

Importantly, the insurer will not require any information regarding your health at that time. So you can have additional mortgage cover without your health affecting the premiums.

Bear in mind that policies with a GIO will have limits on the extra cover and specific timeframes of when you need to contact the insurance company.

Reviewing existing policies

Whenever your personal situation changes, including your mortgage, it is important that any existing life policies are reviewed.

If you have increased your mortgage then it is sensible to consider taking out life cover for the extra amount.

Sometimes this can mean using an existing term insurance policy and just buying some ‘top-up’ cover.

However, it can also be cheaper to get all of the cover from a new insurer (a bit like a remortgage).

Problems can arise if you extend the term of a mortgage as then the old policy will stop before the mortgage is repaid, leaving you short on cover.

Can you have more than one policy? – Yes.

Speak to a financial adviser to work out the best option.

How much cover is needed?

As a minimum, you should look to have death cover for the amount of your mortgage, including any fees added to it.

Depending on your loan to value percentage, some lenders allow you to add fees to your mortgage, rather than paying them upfront. This increases your debt and so needs to be factored in to the life cover. Your mortgage illustration will show these fees, which will normally be the mortgage arrangement/product fee and possibly a higher lending charge.

Let’s say you need a mortgage of £250,000. If you add these fees to the loan, then the amount you actually borrow could be £255,000, an extra £5,000.

To fully protect this mortgage you would need life cover of £255,000.

Level or decreasing?

The choice of whether to have life insurance, or not, is yours.

So the decision about whether to have level cover or decreasing cover, is again yours.

Sometimes affordability will be the overriding factor, but there isn’t a great deal of difference in the monthly cost. Let’s look at the two types of mortgage repayment method:

Full repayment mortgage

Nearly all borrowers will choose the full repayment method when applying for a mortgage. This means that with every monthly payment you are gradually chipping away at the debt.

When you receive your annual mortgage statement, you will see that the balance is gradually going down.

Decreasing mortgage life insurance

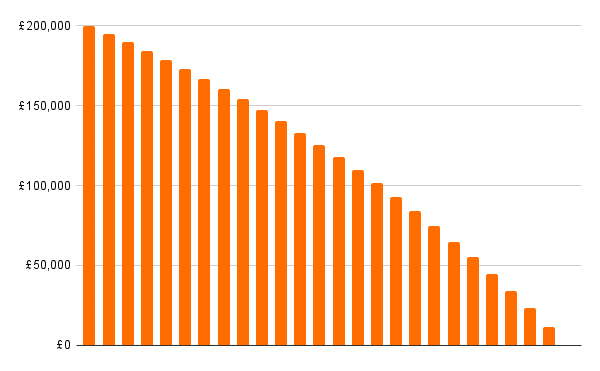

This policy is designed to cover a repayment mortgage, where the mortgage balance goes down each year. Your life cover will automatically go down each year, broadly inline with your mortgage balance. This is the cheapest form of mortgage life insurance.

How does the cover decrease? With decreasing mortgage life insurance the insurer will reduce the cover each year by a certain percentage, or ‘interest rate’. Mortgages don’t go down in a straight line, as you pay more interest each month in the early years and less in later years. The policy is designed to mimic this. But don’t forget that the policy is not linked to your mortgage. So it rarely pays out the exact amount of money needed.

Level mortgage life insurance

Although your mortgage debt gets less each year, some people choose to have the life cover amount stay at the original value, ie level. This means that if you die, the amount of money paid out (after year 1) would be more than the mortgage debt. This is additional money for your family that could help pay funeral costs, credit card bills etc. This policy will be around 10-15% more expensive.

Interest-only mortgage

This is a bit more straightforward. With an interest-only mortgage you are only paying the interest on the loan. None of your payments are reducing the original amount borrowed.

Each year you will see that the mortgage balance is the same as before.

Level mortgage life insurance

Level cover is the only sensible choice for an interest only mortgage, as you need the death cover to not reduce.

Policy options

Some policies will have extra options which you may wish to consider.

Guaranteed Insurability Option

The ability to increase your cover in the future, regardless of your health at that time.

Waiver of Premium

An extra insurance that could help to maintain the policy premiums should you be unable to work due to illness or accident.

Terminal Illness

Terminal Illness Cover could pay out the full amount of death benefit if you are diagnosed with a terminal illness (when life expectancy is less than 12 months) during the policy term.

Critical Illness

Critical illness cover pays out a cash sum should you suffer from one of the specified critical illnesses. These include cancer, heart attack and stroke.

When to apply

You should apply for mortgage life insurance as soon as you have decided on a mortgage product and lender.

This means that you can set the policy up correctly using the right mortgage amount and the repayment term.

Don’t worry, the policy won’t start automatically.

Once the insurance company has finished processing your application and completed the underwriting process they will confirm that your policy has been accepted and also re-confirm the premium and benefits.

You can then notify them of a start date at a later time.

When should the cover start from?

Purchase mortgage – Upon exchange of contracts.

Remortgage – When completion is scheduled for.

What happens to life insurance if you remortgage?

Remortgaging involves transferring your mortgage to a new lender but without moving home.

Many people use this opportunity to borrow extra money or make other changes to the mortgage. Your life cover should be reviewed at the same time, to ensure there is sufficient cover in place.

Nothing will happen to any existing policies you have.

If you borrow more money, or extend the mortgage term, then there will be a need to seek additional cover.