So, you’re thinking of buying a second property. But before you start browsing through listings and getting your heart set on that perfect cottage in the country, there are a few things you need to take into account.

One of the most important is financing – how are you going to pay for it?

There are a number of ways to remortgage in order to get the money you need for another property, and we’re here to help you figure out which one is right for you. We’ll take a look at some of the most popular options and explain the pros and cons so that you can make an informed decision.

So read on, and find out everything you need to know about remortgaging to buy another property!

What is a remortgage?

Remortgaging is the process of taking out a new mortgage secured against your property, replacing your existing mortgage.

It allows you to access the equity in your home without selling it and can offer the opportunity for better interest rates and more favourable loan terms.

Borrowing against your own home is often the cheapest way of getting a loan and banks are keen to lend to homeowners.

It is equally possible to remortgage a second property that you already own. This could be an investment property like a buy to let or a holiday home.

How do you borrow the extra money?

When it comes to borrowing the extra money for remortgaging to purchase a second property, there are several options available. While remortgaging is the most popular, some people find that a secured loan, or second charge mortgage, is more convenient.

What is a secured loan? – A secured loan is a second mortgage taken out against your home while leaving your main mortgage in place. They are a bit more expensive than a remortgage.

However, they are a useful way of borrowing if for some reason you are unable to qualify for a remortgage. You would take out this second mortgage to raise the extra money needed.

Remortgaging – Here you apply for a larger, capital raising mortgage, which will be used to pay off your current lender and then the balance is available to put towards a further property. This requires a full mortgage application to the new lender, along with the normal documents needed for a remortgage (proof of income, ID, etc).

How much can you borrow?

The amount you are able to borrow will depend on a number of factors, such as your current mortgage balance, the value of your home, your income, and how much equity you have available.

By borrowing money in this way you are raising capital, or capital raising. It’s also possible to borrow extra money in this way for a new car, home improvements or to consolidate and pay off other more expensive debts.

All lenders will work to a maximum loan to value, or LTV. This is the maximum percentage of your property value that they will go up to.

For example. If your home is worth £300,000 and the bank is willing to lend up to 90% LTV, this would equate to £270,000. This figure would have to include fully repaying the current mortgage.

When borrowing against your own home there are plenty of lenders offering 90% loan to value at competitive rates. But don’t forget that you also need to have the income to qualify and afford the higher amount.

When you capital raise you are accessing the equity that comes from an increased house value.

Capital raising for a deposit

It is unusual for someone to capital raise enough money to then buy a property outright. (although this is possible).

Most will remortgage so they have enough for a deposit and the other upfront purchase costs such as legal fees and stamp duty.

The money raised is used as a deposit on the additional property, and then a new mortgage is arranged for the remaining funds needed.

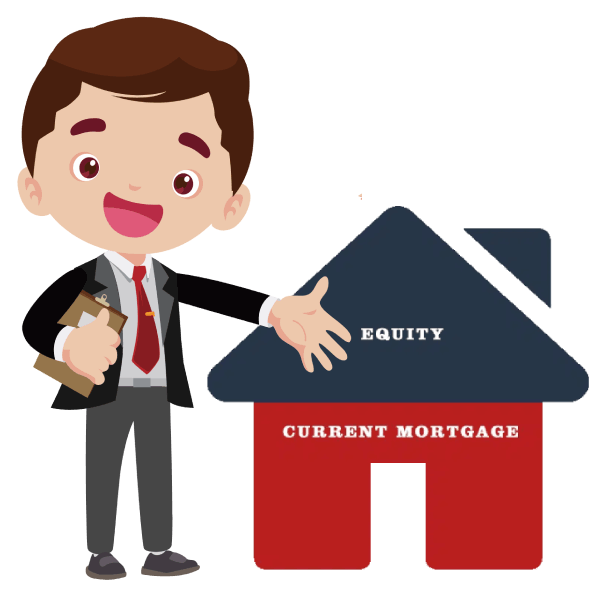

What is equity?

Equity, or home equity, is the difference between the market value of a property and the amount outstanding on any loans secured against it.

In other words, it is the portion of a property that you actually own outright.

Equity can be used in various ways and is often referred to as an additional collateral for securing finance or for releasing additional funds for use elsewhere.

It can be used to secure a further loan when remortgaging for a second house or, alternatively, it can be accessed through equity release products such as lifetime mortgages or home reversion plans.

If you owned a property worth £300,000 with a £200,000 mortgage then your equity would be £100,000.

Why do I need equity to remortgage?

A mortgage is a loan that is secured against a property. This means that the lender registers a legal charge on the property deeds, giving them extra security in the event that you stop making the monthly repayments. This security means that they can lend large sums of money at low rates.

A bank will only lend against the available equity in a property and then only up to a maximum LTV percentage. In the example above we used 90% LTV.

So with a property worth 300K and a mortgage of 200K, you would be able to re-mortgage for 270K and capital raise £70,000 from the available equity.

Can you remortgage a house without a mortgage? – Yes you can. A property that you own without any mortgage would be called an unencumbered property.

Remortgaging when your house value has increased

Can you release equity on an inherited house?

What type of property can you buy?

You can buy most types of property, but this will be something that the lender is particularly interested in and it will affect the remortgage terms on offer.

With the extra funds you raise you could buy a:

MUFB

A buy to let on steroids! A multi-unit freehold block (MUFB) is a few dwellings contained within one freehold property.

Airbnb

An Airbnb can be likened to a holiday let or a serviced accommodation property. Either way a specialist mortgage is needed.

Commercial property

A commercial property will be let to a business, often on a long lease of 5 years or more.

Plot of land

Maybe it’s a plot of land to build on or your own private woodland or forest.

Uninhabitable

You cannot get a standard mortgage on an uninhabitable house. But paying with cash gets around this problem.

CONTACT A REMORTGAGE EXPERT

If you wish to investigate your re-mortgage options we can put you in touch with a fully qualified whole of market mortgage broker.

Can you have two mortgages?

Yes you can have two mortgages.

You might be surprised to learn that there isn’t actually a limit on the number of mortgages that a person can have.

You would normally have one residential mortgage for your home and then any other mortgages would depend on the property usage. For example; buy to let mortgage for a let property or second home mortgage for a holiday home.

It’s fairly common for us to deal with portfolio landlords that own dozens of properties, some have portfolios of more than 50, and each property has it’s own mortgage.

For each additional mortgage you would need to meet the lender’s criteria and pass their credit and affordability checks.

Can you remortgage to buy another property with cash?

Yes this is possible.

It very much depends how much the additional property costs and how much equity you have available. And of course, you need to have the financial status to allow this to happen.

As an example:

You have a home worth £500,000 with a £100,000 mortgage. (£400,000 equity).

You wish to purchase a second property for £150,000.

This would require a remortgage for £250,000, which would raise £150,000 as ‘cash’.

This money would be used to purchase the additional property outright, as a cash buyer.

How do I get the best advice?

This guide has shown you only some of the options available to capital raise and buy another property. To get the best advice, and the best remortgage options, we would suggest speaking with an independent remortgage broker.

There are many advantages to using a mortgage broker and they will have the experience and knowledge to plan the best way of raising the money you need. Independent brokers aren’t restricted in the number of lenders that they can consider, so your options will be sourced from the whole mortgage market.

One important aspect to discuss with them is early repayment charges, or ERCs. These are exit fees charged by lenders when you repay their mortgage before the agreed date. Your broker will be able to work out how much these may be, not everyone gets charged an ERC, and then find the most cost effective way forward for you. Occasionally it may be necessary to remortgage early and then these fees are payable.

Respect Mortgages works with one of the longest established firms of independent mortgage broker in the UK.

Winners of many awards, with expert advisers covering all of the UK, they provide high quality advice wherever you are located.

Calculator

Loan to Value (LTV) Calculator

Loan to Value or LTV is an expression used by all mortgage and secured loan lenders. It is a pretty simple concept but not everyone is aware of what it is and how to work it out.

Our simple online calculator does all of the hard work for you, so you can see the LTV in just a few seconds.