The traditional term for repayment of a UK mortgage is 25 years. Longer and shorter terms have been available but this seems to be a length of time that borrowers are comfortable with.

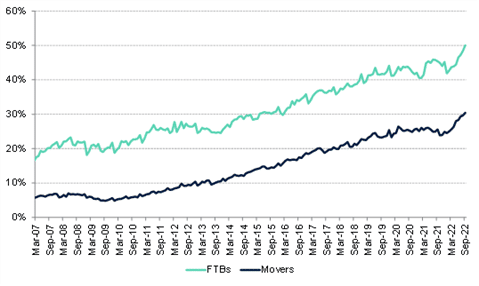

Recent research has discovered that half of all first time buyers are now choosing a mortgage term of 30 years, or more.

This news comes from UK Finance’s latest Household Finance Review which analysed mortgage applications from July to September 2022.

Choosing a longer mortgage term is a trend that began after the global financial crisis, which happened around 2008/2009. And as you can see from the graph below, this trend really picked up during and after Covid.

So should you get a 30 year mortgage term?

The way that a mortgage is set up will reflect the needs and aims of a particular borrower. It depends on your personal circumstances and objectives.

For example, if you are in a position to make higher than average monthly payments then it may be worth considering a shorter mortgage term so you can pay off the debt faster and save money in interest over the life of the loan. On the other hand, if your budget is tight and you need to spread the cost of your loan over a longer period, then a 30 year term could be suitable.

When choosing an interest rate some borrowers prefer the security that comes with a fixed rate, while others are happy to go with a tracker deal, which is cheaper but not so predictable.

As most first-time buyers will move house well before their first mortgage reaches the end of its term, the cost over time may be a more minor consideration for many.

How does the term affect a mortgage?

The term of a mortgage will directly affect the monthly cost of a repayment mortgage.

If you take a very simple example of a £250,000 mortgage. It would cost a lot more each month to repay this back over 20 years than it would to pay it back over 30 years. This is because you are compressing all of the debt repayment into a shorter period.

Here’s some figures to explain further:

| 250K Repayment Mortgage | ||||

|---|---|---|---|---|

| 2% | 3% | 4% | 5% | |

| 10 years | £2300 | £2414 | £2531 | £2651 |

| 15 years | £1608 | £1726 | £1849 | £1976 |

| 20 years | £1264 | £1386 | £1514 | £1649 |

| 25 years | £1059 | £1185 | £1319 | £1461 |

| 30 years | £924 | £1054 | £1193 | £1342 |

As you can see the 20 year repayments are £340 more per month than for the 30 year term.

What effect does the term have on an interest only mortgage?

Interest only mortgages work differently from repayment mortgages.

With an interest only mortgage you are just liable for the interest, so the monthly payments are lower than the equivalent capital and interest loan. But bear in mind that you will still need to pay back the full amount of your loan at the end of the term.

So if you were to take out an interest only mortgage, then the term will have no direct effect on your monthly payments. Because the payments are quite a bit lower than the equivalent repayment mortgage, your mortgage affordability is improved. However, lenders are not keen on approving interest only loans.

Having a longer term will give you more time to accumulate the capital to repay the loan. Prolonging the eventual repayment actually makes the mortgage more expensive as the interest will need to be paid for a longer period of time.

And remember that with an interest only mortgage the balance stays the same, so you are always paying the ‘full’ amount of interest.

If the interest-only option is still needed then a better way would be to make adhoc lump sum repayments as and when these become affordable. This will have the effect of reducing the interest charges for the remaining term.

| 250K Interest Only Mortgage | ||||||

|---|---|---|---|---|---|---|

| 2% | 3% | 4% | 5% | 6% | 7% | |

| 10 years | £417 | £625 | £833 | £1041 | £1250 | £1458 |

| 15 years | £417 | £625 | £833 | £1041 | £1250 | £1458 |

| 20 years | £417 | £625 | £833 | £1041 | £1250 | £1458 |

| 25 years | £417 | £625 | £833 | £1041 | £1250 | £1458 |

| 30 years | £417 | £625 | £833 | £1041 | £1250 | £1458 |

So with an interest only mortgage it’s important to think about how you repay an interest only mortgage? and what happens when my interest only mortgage ends?

Why would a first time buyer choose a longer mortgage term?

Buyers are borrowing for longer due to issues with affordability and the decline of interest-only mortgages. Some first time buyers feel safer opting for a longer mortgage term, as it gives them a lower and more affordable monthly payment.

And if it’s a fixed rate mortgage, then they have the security of knowing the payment will stay the same for the duration of the deal. This can be helpful in budgeting and managing your finances.

First-time buyers are often on tight budgets but with the cost of housing being so high in certain areas, larger mortgages are needed to keep up with the price rises. A longer term mortgage can provide the opportunity to get onto the property ladder, by bringing down the monthly cost.

Our easy to use online calculator can help you to work out how much you could borrow on your residential mortgage, just by entering your income.

You may find this interesting: Is a marathon mortgage right for you?

The extra costs of longer term mortgages

It can be significantly more affordable in the short term to take out a longer mortgage. The big problem is that it will take you more time to fully pay off the loan and you’ll end up paying more in interest.

So lowering your monthly mortgage repayments doesn’t add up to overall savings.

Continuing with our example above, over the traditional 25 year term you will have paid £188,443 in interest.

By increasing the term to 30 years means that you will have paid £233,139 in interest.

So that extra five years has cost £44,696.

Existing mortgage

If you already have a mortgage in place then you may be wondering “Can I extend my mortgage term?“. And the answer, is yes you can. You will either need to approach your lender and ask if you can do this, or look to remortgage to a new lender.

You will find more useful information in our article: What’s the longest mortgage term you can get?

Award winning service

Independent mortgage advice

Mortgage experts

How your age impacts a longer term mortgage

Over the last ten years or so, lenders have been increasingly willing to allow people to borrow into their retirement ages.

It used to be the case that your mortgage term finishes at your specified retirement age, or perhaps the state pension age. Slowly lenders have become more relaxed about this and have extended the terms. We now have a new range of later-life mortgages, suitable for those age 55 or over.

The reason why 50% of first-time buyers can and do choose a 30 year term is because they are among the youngest age group of homeowners. They have the longest period of time in front of them before retirement.

Should I pay off my mortgage before I retire?

Ideally you should aim to pay off your mortgage before you retire.

The longer your mortgage term, the more interest you will pay overall. Of course it is not possible for everyone to do this, but if you are able to then it could be a great way of making sure that when you retire your finances are in good shape and free from those large mortgage payments.

Making additional repayments alongside your regular payment can help reduce the amount of time you need to pay off your mortgage. Investing money or other capital into paying off the loan with lump sum payments can also make a significant difference.

Mortgage lenders aren’t keen to lend into retirement and for those who do, there can be additional affordability assessments and criteria required to prove you can afford the mortgage.

Ultimately, when it comes to choosing a mortgage term, it’s a balancing act between short-term affordability and longer-term costs. If possible, aim for the shortest term which will still allow you to meet all of your other financial commitments whilst keeping up with your repayments. And always remember to make use of any extra funds available for overpayments and lump sums as this could significantly reduce the length of your mortgage term.

In summary

The vast majority of borrowers will need to choose a mortgage that is affordable for them. To make the monthly payments lower (for the same mortgage) there’s only 2 options: 1) Make the mortgage term longer, 2) Have some or all of the loan as interest-only.

As a first time buyer you may need a 30 year term to get the repayments down to an affordable amount. That allows you to stop paying rent and get onto the property ladder. Yes there’s more interest charged if you run the mortgage for the full 30 years, but you will also have benefitted from rises in property prices.

Lenders are now more willing to offer longer repayment terms, even though these may creep into the retirement zone of age 65 and over. It’s important for all borrowers to consider how they will deal with the mortgage debt should this turn into reality.

As always, you can get professional advice and an experienced perspective by contacting an independent mortgage broker.